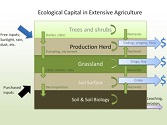

Abstract

Agriculture relies on efficient transformation and regeneration of ecological capital to sustainably produce a range of life-supporting goods and services. An improvement in the ability to account for ecological capital in agriculture may assist recognition, avoidance and reversal of its depletion. This paper investigates current conventions of accounting for biological, productive and land-related assets to conceptualise a way of incorporating ecological capital in the accounting framework of business entities. A conceptual framework for ecological capital in agriculture is used to link intermediate and productive biological assets to inflows and outflows of economic benefit. An Ecological Balance Sheet (EBS) is proposed as a means to deliver a more complete representation of an agricultural entity’s total equity and to keep records of where changes to ecological asset accounts cause flows of expenditure. Methods and strategies to design, develop and continually improve the use of the EBS in agriculture are suggested to help other researchers further explore this concept.

Abstract Download article here Agriculture relies on efficient transformation and regeneration of ecological capital to sustainably produce a range of life-supporting goods and services. An improvement in the ability to account for ecological capital in agriculture may assist recognition, avoidance and reversal of its depletion. This paper investigates current conventions of accounting for biological, productive and land-related assets to conceptualise a way of incorporating ecological capital in the accounting framework of business entities. A conceptual framework for ecological capital in agriculture is used to link intermediate and productive biological assets to inflows and outflows of economic benefit. An Ecological Balance

Abstract Download article here Agriculture relies on efficient transformation and regeneration of ecological capital to sustainably produce a range of life-supporting goods and services. An improvement in the ability to account for ecological capital in agriculture may assist recognition, avoidance and reversal of its depletion. This paper investigates current conventions of accounting for biological, productive and land-related assets to conceptualise a way of incorporating ecological capital in the accounting framework of business entities. A conceptual framework for ecological capital in agriculture is used to link intermediate and productive biological assets to inflows and outflows of economic benefit. An Ecological Balance